Nobody Told Gen Z That Looking Rich and Being Rich Are Opposite Things

There is a generation walking around in ₹15,000 sneakers, financing cars they cannot actually afford, eating at restaurants that cost more than their parents' entire weekly grocery run — and feeling completely normal about all of it. Gen Z is not reckless. They are not stupid. They are not even particularly irresponsible when you look at them as individuals. But they are the first generation in human history to grow up in a world where looking wealthy became cheaper, easier, and more socially rewarded than actually being wealthy. And almost nobody warned them that those two things are not just different — they are actively working against each other.

This is not a lecture about avocado toast or overpriced coffee. This is about a structural trap that an entire generation has walked into — one built by banks, brands, social media platforms, and fintech apps — and why the people most at risk are the ones who feel like they are doing fine because their lifestyle looks good.

The Illusion Was Built for You Specifically

The aesthetics of wealth have never been more accessible. Fast fashion brands deliver the look of luxury at a fraction of the price. Car financing has made a ₹12 lakh vehicle feel like a ₹9,500 per month decision. Buy Now Pay Later apps have turned a ₹6,000 impulse purchase into six easy instalments that barely register. Social media has made the visual display of wealth into a daily social currency — something you perform, curate, and post, not something you quietly accumulate over decades.

None of this happened by accident. Every single one of these systems was deliberately designed to make spending feel smaller, easier, more normal, and more socially necessary than it actually is. The EMI frame makes a ₹10 lakh purchase feel like a ₹8,000 question. The BNPL frame makes a ₹4,000 purchase feel like four ₹1,000 questions spread across four months. The social media frame makes every purchase a performance that generates likes, validation, and the dopamine hit of seeming successful to people whose opinion you may not even actually value.

Gen Z did not create this environment. They were born into it. But they are the ones paying for it — quite literally.

What the Spending Actually Looks Like Up Close

When you break down the monthly finances of an average urban Gen Z professional earning ₹45,000–65,000 a month, the picture becomes uncomfortable very quickly.

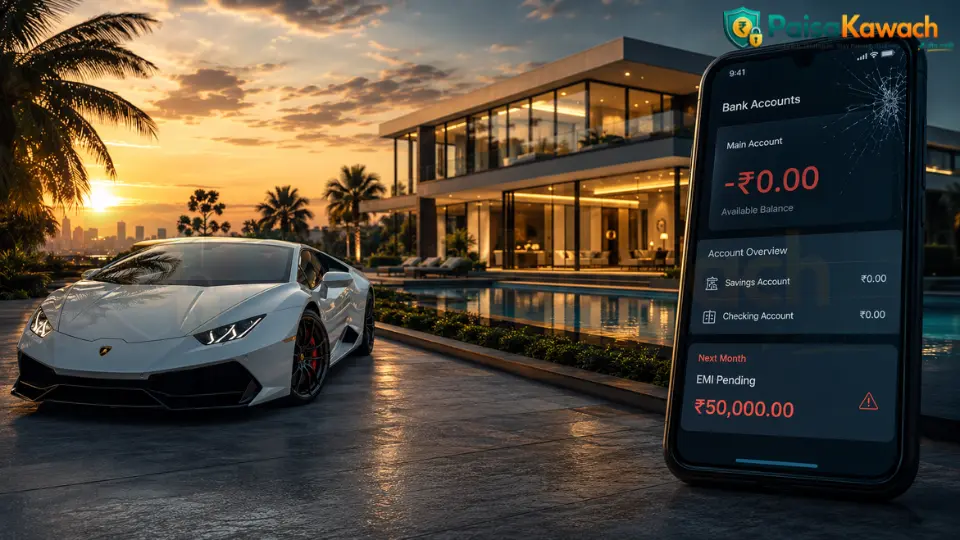

- A mid-range car on EMI — ₹10–14 lakh financed over 5 years — costs ₹18,000–25,000 per month in EMI alone, before insurance, fuel, parking, and maintenance, which together easily add another ₹8,000–12,000. That is ₹26,000–37,000 a month on a vehicle on a salary of ₹45,000. The math does not need commentary.

- Food delivery and eating out 4–5 times a week — average order ₹350–600 on Zomato or Swiggy, plus 2–3 café or restaurant outings a week at ₹500–1,200 each — comfortably crosses ₹8,000–14,000 per month. Annually, that is between ₹96,000 and ₹1,68,000 spent on food outside the home.

- Subscriptions that feel small individually — Netflix ₹649, Spotify ₹119, Amazon Prime ₹1,499 annually, iCloud storage ₹75, Zomato Gold ₹149, gym membership ₹1,200, one or two app subscriptions — add up to ₹3,500–5,500 per month that most people cannot immediately account for when asked where their money went.

The Generation With the Most Financial Content Is Also the Least Financially Secure

This is the paradox that nobody wants to talk about directly. Gen Z has access to more personal finance content than every previous generation combined. There are thousands of YouTube channels dedicated to money management. Instagram is full of finance influencers breaking down SIPs, index funds, tax saving, and compound interest in 60-second reels. Reddit communities like r/IndiaInvestments have hundreds of thousands of members sharing detailed financial advice. There are podcasts, newsletters, Twitter threads, and entire media companies built around teaching young people how to handle money.

And yet, by almost every measurable metric, Gen Z is saving less, investing less, and carrying more consumer debt than Millennials did at the same age — who themselves were doing worse than Gen X did at the same age. The information was never the missing ingredient. Something else is going on.

The answer is environment. Human behaviour is shaped far more by environment than by knowledge. You can know, intellectually, that smoking is lethal — and still smoke if everyone around you smokes and cigarettes are available at every corner. You can know, intellectually, that overspending on lifestyle is destroying your financial future — and still do it if your entire social environment is structured around that spending, if every digital platform you use is optimised to trigger purchasing decisions, and if the social cost of not participating in the lifestyle feels higher than the abstract future cost of not saving.

Why All the Financial Content in the World Isn't Moving the Needle

The content exists. The behaviour hasn't changed. Here is why that gap persists.

- For every one personal finance reel a Gen Z user sees, the algorithm serves them approximately 30–50 lifestyle, fashion, food, travel, and consumer product reels — all of which are either directly sponsored or culturally normalising the kind of spending the finance reel just told them to avoid. The counter-programming is not subtle. It has a billion-dollar budget.

- Zero-cost EMI and BNPL have fundamentally altered the psychology of affordability. When something is split into small monthly payments, the brain does not process it as the full purchase price — it processes it as the monthly number. Research in behavioural economics consistently shows that people are willing to spend significantly more in total when payments are spread out, even when the total cost is clearly visible. The brain discounts the future cost in favour of the immediate smaller number.

- Social spending is now publicly visible in a way that has no historical precedent. For most of human history, you only knew what your immediate neighbours and friends owned and spent. Today, you have real-time visibility into the consumption patterns of hundreds or thousands of people — what they are eating, where they are travelling, what car they just bought, what sneakers they are wearing. This triggers social comparison at a scale the human brain was never built to handle, and the default response is to match or exceed what you see.

The Real Price Tag on Looking Rich

Here is the number most people never calculate — not the cost of any individual purchase, but the opportunity cost. Every rupee spent on lifestyle signalling is not just a rupee gone. It is a rupee that will never compound. And compounding is the only financial concept that matters at 23, 25, or 28 years old, because time is the one ingredient you have that no amount of money can later buy back.

Take a straightforward example. Two people, both 23 years old, both earning ₹50,000 a month. Person A buys a car on EMI — ₹12,000 per month for 5 years, plus lifestyle upgrades that absorb another ₹8,000 monthly. Person B drives a second-hand scooter, keeps lifestyle costs lean, and invests ₹20,000 per month in a basic index fund. By 28, when Person A's car loan ends, Person B has been investing for 5 years. At a conservative 12% annual return, that ₹20,000 monthly investment over 5 years is already worth approximately ₹16.5 lakh. Person A has a depreciating car worth maybe ₹5–6 lakh and zero invested assets.

Now both of them start investing ₹20,000 a month at 28. By 50, Person B — who started at 23 — has approximately ₹4.8 crore. Person A — who started at 28 — has approximately ₹2.6 crore. Same salary. Same investment amount. Same return rate. The only difference is 5 years of starting age. The cost of that car, in retirement wealth terms, was not ₹7.2 lakh in EMIs. It was ₹2.2 crore in compounding. Nobody shows you that number at the showroom.

The Hidden Costs That Never Make It Into the Budget

Beyond opportunity cost, lifestyle inflation carries several expenses that most people systematically underestimate or ignore entirely.

- Depreciation on consumer goods — cars, gadgets, fashion — is brutal and silent. A ₹12 lakh car loses approximately 15–20% of its value in the first year and 10–15% every year after. By year 5, it is worth ₹4–5 lakh. You paid ₹12 lakh plus interest. The asset is worth a third of what you paid. That loss never appears as a line item in anyone's monthly budget, but it is as real as any EMI.

- Lifestyle maintenance costs scale with lifestyle level. A higher-end car requires higher-end servicing, higher insurance premiums, higher parking costs, and higher fuel consumption. Eating at better restaurants means tips, travel to those restaurants, drinks with the meal, and dessert. Every lifestyle upgrade comes with a tail of smaller expenses that nobody budgets for but everyone pays.

- The social escalation trap — once you establish a certain lifestyle level in your social circle, stepping back from it carries real social cost. You stop being invited to certain things. You feel out of place. The lifestyle becomes a floor, not a ceiling, and the only direction available is up.

What Actually Being Wealthy Looks Like at 25 — And Why It Photographs Terribly

Real financial security at 25 is profoundly unglamorous. It looks like a term insurance policy nobody posts about. It looks like a health insurance plan with a decent sum insured that you hope to never use. It looks like a SIP running quietly in the background every month, automatically, without drama. It looks like no car loan, or a modest second-hand vehicle bought outright. It looks like an emergency fund sitting in a liquid fund or high-yield savings account, capable of covering 4–6 months of expenses, completely untouched. It looks like a credit card that is paid in full, every single month, without exception.

None of that photographs well. None of it generates Instagram content. None of it impresses anyone at a party. But every single one of those things is a foundation — something you build on. Every ₹15,000 sneaker and every financed car upgrade is the opposite. It is a subtraction disguised as an addition, a cost disguised as a statement, a hole in the foundation disguised as a floor.

The people who understand this early — not intellectually, but behaviourally, in their actual daily spending decisions — are the ones who will have options at 35, 40, and 50 that the rest of their generation simply will not have. Not because they were smarter. Not because they earned more. Because they understood the difference between performing wealth and building it, and they chose building.

What the Five-Year Divergence Actually Looks Like

The gap between the two paths does not become visible immediately — which is exactly why the lifestyle path feels safe. The consequences are delayed. The compounding is silent. But by the time the gap becomes visible, it is very difficult to close.

- At 25, both paths look roughly similar — same salary, similar lifestyle on the surface. The person building wealth just has less visible stuff and more invisible assets growing in the background.

- At 30, the divergence starts to show. One person has an investment portfolio worth ₹15–25 lakh, no consumer debt, and genuine financial flexibility. The other has a depreciating car, a lifestyle that requires their full salary to maintain, and approximately ₹0 in invested assets.

- At 35, the gap is a chasm. One person has the option to take a career risk, start something, take a pay cut for better work, or simply feel financially secure. The other is on a treadmill — earning more but spending more, always one job loss or medical emergency away from serious financial stress.

This Is Not About Deprivation — It Is About Knowing What You Are Actually Buying

The point of all of this is not that Gen Z should stop enjoying their 20s. It is not that eating out is evil or that wanting a nice car is morally wrong. The point is something simpler and more uncomfortable: most of the spending that is draining Gen Z accounts is not actually bringing the satisfaction it promises. It is bringing social validation, anxiety relief, and FOMO management — which are real psychological needs, but extremely expensive ones to meet through consumption.

The sneakers do not make you feel successful for more than a week. The car stops feeling special after three months. The restaurant meal is forgotten by Tuesday. But the EMI runs for 60 months. The opportunity cost compounds for 30 years. The pattern — spend first, feel briefly validated, return to baseline, spend again — is exactly the cycle that the entire consumer economy is built to perpetuate, because a generation that actually saved and invested aggressively would be catastrophic for quarterly revenue figures.

Understanding that you are the product — that your spending impulses are being carefully engineered by systems with far more data about your psychology than you have about theirs — is not paranoia. It is the beginning of actually being in control of your financial life rather than just feeling like you are.

Three Shifts That Change the Entire Equation

Not rules. Not restrictions. Just three reframes that change the way individual spending decisions actually feel.

- Convert every significant purchase into its compounding equivalent before buying. That ₹15,000 sneaker invested at 12% annually for 25 years is ₹2.7 lakh. You are not buying sneakers. You are choosing sneakers over ₹2.7 lakh at 50. That framing does not mean you never buy the sneakers — but it means you are making the actual decision, not a disguised version of it.

- Separate social spending from personal enjoyment. Before any significant purchase, ask honestly: would I still want this if nobody could see it, post about it, or know I own it? If the answer is no, you are not buying a product. You are buying an audience reaction. That is fine if you know that is what you are doing — but it should be a conscious choice, not an autopilot one.

- Automate the saving before the spending happens. The single most effective financial behaviour change is not budgeting or tracking — it is making investment automatic and moving it before you ever see the money. A SIP that pulls on salary day, before any discretionary spending occurs, removes the decision entirely. You cannot spend money that is already gone. The lifestyle adjusts to what remains, and within 2–3 months, most people stop noticing the difference.

The Uncomfortable Truth Nobody in the Room Is Saying

Gen Z is the most financially educated generation in history and among the least financially secure. That is not a failure of intelligence. It is a failure of environment — an environment that was specifically designed, at enormous expense and with extraordinary psychological sophistication, to keep them spending.

The brands know your spending triggers better than you do. The apps know exactly which notification to send at exactly which moment to get you to open the app and buy something. The banks know that zero-cost EMI makes you spend 30–40% more in total than you would on a cash purchase. The social media platforms know that showing you your peers' consumption habits is the single most effective way to drive your own consumption.

None of them are going to tell you this. None of them have any incentive to. The only people with an incentive to tell you are the ones who are not trying to sell you anything — and those people are, unfortunately, much quieter than the ones who are.

Looking rich is available to almost everyone in 2026. Being rich — actually, quietly, fundamentally financially secure — is available to anyone who understands the difference early enough to act on it. That window is open widest between 22 and 30. Every year it gets a little harder to close the gap. The generation that figures this out first, and acts on it first, will look indistinguishable from everyone else at 25 — and completely different from everyone else at 45.

Keep Reading: More Insights You Might Like

Comments

No comments yet. Be the first to comment!