Walmart Q4 FY2026 Earnings — Strong Results but Cautious Outlook Signals a Softening US Consumer

On paper, Walmart's fourth-quarter results looked like a win. Revenue topped estimates, earnings came in ahead of Wall Street's expectations, and the company's board authorised its largest-ever share repurchase programme. But in the hours after the February 19, 2026 earnings release, Walmart's stock fell sharply — because experienced investors know the real story is never just about what a company earned last quarter. It's about what they expect to earn next.

And on that front, the world's largest physical retailer delivered a sobering message. Walmart's full-year adjusted EPS guidance of $2.75 to $2.85 fell significantly short of the $2.96 analysts had pencilled in. For a company that serves approximately 270 million customers every single week across more than 10,750 locations globally, a cautious outlook isn't just a corporate footnote — it's a signal about the state of the global consumer.

📊 Snapshot — Walmart Q4 FY2026 Key Facts

- Q4 Revenue: $190.7 billion — up 5.6% year-over-year, beat estimate of $190.49B

- Adjusted EPS (Q4): $0.74 — narrowly beat consensus of $0.73

- Global eCommerce Growth: +24% year-over-year

- Walmart Connect (Advertising): US segment up 41%

- FY2027 EPS Guidance: $2.75–$2.85 vs analyst expectation of $2.96

- FY2027 Net Sales Growth Guidance: 3.5%–4.5%

- Share Buyback: $30 billion — largest in company history

- Annual Dividend: Raised 5% to $0.99/share — 53rd consecutive annual increase

- WMT Stock Reaction: Fell approximately 3% following the guidance miss

What Walmart Got Right — And It Was Plenty

To be fair to Walmart, the underlying business delivered in nearly every dimension that matters for long-term investors. Revenue of $190.7 billion for the quarter surpassed expectations, driven by a powerful combination of foot traffic, digital growth, and an expanding high-margin advertising business.

Global eCommerce sales surged 24% year-over-year, with US eCommerce reaching full-year profitability for the first time — a milestone the company has been working toward for years. Walmart Connect, the company's advertising division that monetises its massive customer data footprint, grew 41% in the US. These are not the metrics of a struggling retailer; they are the metrics of a business successfully transforming itself from a box-shifting giant into a tech-forward, margin-expanding platform.

The $30 billion share repurchase authorisation — replacing a prior $20 billion programme from 2022 — and the company's 53rd consecutive annual dividend increase underscored management's confidence in Walmart's long-term cash generation. Operating cash flow for the full fiscal year hit $42 billion, with free cash flow growing 18%.

The Guidance Miss — Why Markets Reacted So Sharply

Despite all of the above, Walmart's stock fell roughly 3% in the aftermath of the release — and that reaction tells you everything about where investor attention is focused right now. The FY2027 adjusted EPS guidance of $2.75–$2.85 was not just a modest shortfall. It was a meaningful gap below the $2.96 consensus, and it arrived at a moment when markets are already on edge about the direction of US consumer spending.

Walmart's CFO was unusually candid about the reason, citing what he called a "somewhat unstable backdrop" and signalling that the company was choosing to start the year conservatively. The company also flagged a meaningful headwind from pharmaceutical pricing legislation — a 100 basis point drag on sales growth from maximum fair pricing rules in the pharmacy segment — and noted that drug pricing legislation creates real uncertainty for its operating income trajectory.

For investors who watch Walmart as the single most reliable barometer of US consumer health, this matters enormously. Walmart is not a luxury retailer insulated from economic cycles. It serves everyday Americans buying groceries, household essentials, and clothing. When Walmart management says the backdrop is unstable, it is speaking from a dataset of 270 million weekly customer interactions — a sample size no economist or analyst can match.

The Amazon Milestone — A Historic Shift in Retail

Buried in this week's earnings context is a landmark development that deserves its own spotlight. For the first time in history, Amazon has overtaken Walmart as the world's largest company by annual revenue. Amazon reported $716.9 billion in revenue for calendar year 2025, compared to Walmart's $713.2 billion — ending Walmart's 13-year reign at the top of the global revenue rankings.

While Walmart remains dominant in physical retail and grocery — areas where Amazon continues to struggle for meaningful share — the crossing of this threshold reflects Amazon's relentless expansion in high-growth, high-margin businesses like AWS cloud computing, digital advertising, and third-party marketplace services. It is a symbolic moment as much as a financial one, marking how dramatically the centre of gravity in global commerce has shifted in a single decade.

What This Means for Investors and Global Markets

Walmart's cautious outlook does not exist in isolation. It lands alongside January retail sales data that came in flat, FOMC minutes this week revealing a surprisingly hawkish Fed tone, and oil prices surging on geopolitical tensions with Iran. The combination paints a picture of a US economy that is still growing, but growing with less conviction than markets had priced in entering 2026.

For global investors, the ripple effects are real and varied. A softening US consumer reduces import demand, which puts pressure on export-driven economies including those in Asia and emerging markets. For Indian companies with US revenue exposure — particularly in IT services, textiles, and pharmaceuticals — Walmart's cautious tone is a watchlist item, not a crisis, but one worth monitoring.

Closer to home, Target is set to report in early March and is currently facing a projected 10% year-over-year decline in EPS according to pre-earnings analyst models. If Target's results confirm the consumer stress signals Walmart has flagged, the narrative around US consumer health could deteriorate meaningfully in the weeks ahead.

Sector Comparison — How Walmart Stacks Up

Within the retail sector, Walmart continues to outperform peers by a wide margin. Its eCommerce profitability, advertising growth, and automation-driven margin expansion differentiate it sharply from traditional brick-and-mortar rivals. Approximately 75% of its recent market share gains have come from households earning over $100,000 annually — a demographic shift that reduces Walmart's historical vulnerability to lower-income consumer stress.

By contrast, Amazon's Q4 revenue of $213.4 billion came with a slight earnings miss, as its $200 billion capital expenditure plan for 2026 — focused heavily on AI infrastructure and AWS — continues to compress near-term margins. Both giants are investing aggressively in automation and AI, but Walmart's approach is more operationally grounded — focusing on supply chain efficiency and same-day delivery from existing stores — while Amazon is making bigger, longer-horizon bets on cloud and AI infrastructure.

What to Watch Next

Several near-term catalysts will either validate or challenge Walmart's cautious guidance in the weeks ahead:

- Today (Feb 20): US Q4 GDP advance estimate and December PCE inflation — the Fed's preferred price gauge — both release today and will set the macro context around consumer spending and rate trajectory

- Early March: Target's Q4 earnings — a critical cross-check on US consumer health signals from Walmart

- February 25: Nvidia earnings — will determine whether AI infrastructure spending remains a growth engine or shows its first signs of plateauing

- March Fed Meeting (Mar 18): Currently showing a 94% probability of a hold — any shift in this probability following today's PCE data will be significant for all rate-sensitive equities globally

- Walmart Connect trajectory: Investors will watch whether the advertising arm can sustain its 40%+ growth rate, as this high-margin segment is the key to Walmart exceeding its own conservative guidance

Walmart has consistently proven that it can outperform its own guidance — management explicitly said their goal is to exceed the numbers they issued. But in a world where geopolitical tensions are lifting oil prices, the Fed is staying hawkish, and flat retail sales are spooking markets, the burden of proof in 2026 is higher than it has been in years. The world's largest retailer just told us to temper our expectations — and the market, for once, is listening.

Keep Reading: More Insights You Might Like

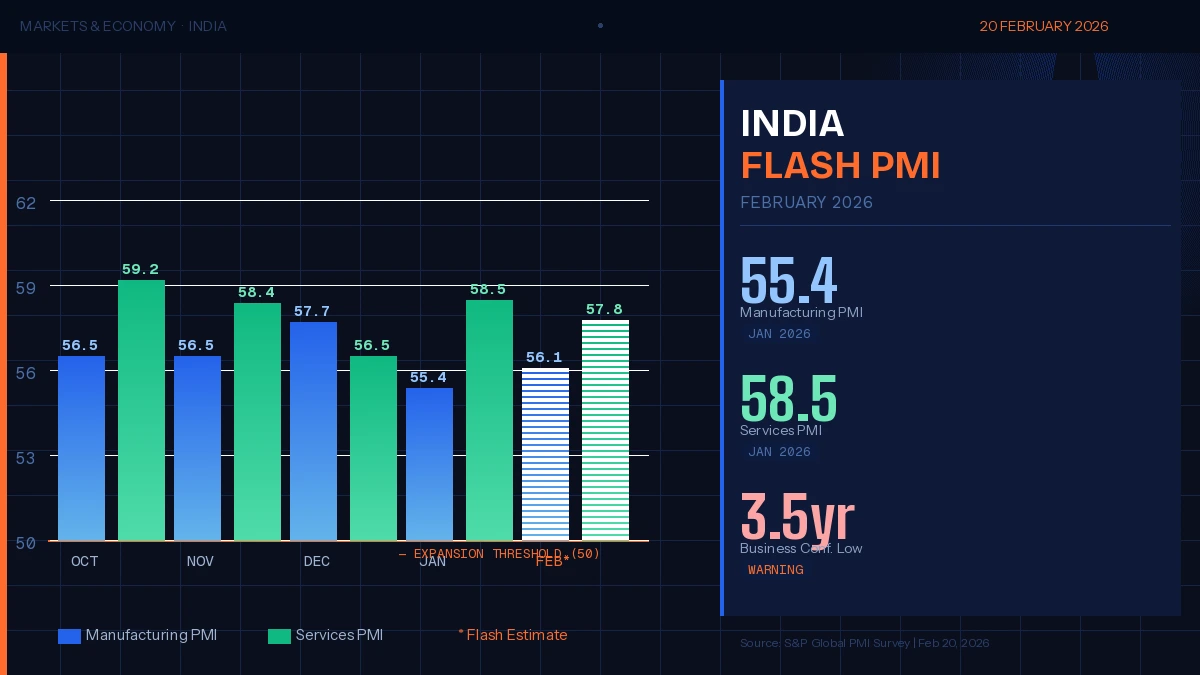

India Flash PMI February 2026 — Is the Growth Momentum Holding or Starting to Slip?

Next →

India Flash PMI February 2026 — Is the Growth Momentum Holding or Starting to Slip?

Next →

RBI May Inject ₹5 Lakh Crore Liquidity in FY27 to Support Credit and Market Stability

RBI May Inject ₹5 Lakh Crore Liquidity in FY27 to Support Credit and Market Stability

Comments

No comments yet. Be the first to comment!